A New Dawn for Ghana’s Economy

In 2025, Ghana witnessed a pivotal moment in its economic journey. The year marked the beginning of a long-awaited reset that brought about significant changes and positive outcomes for the nation’s financial landscape.

Economic Growth Rekindled

The economy experienced a robust rebound. Gross Domestic Product (GDP) grew by 6.1 percent in the first three quarters of 2025, surpassing the 5.7 percent growth recorded during the same period in 2024. This was the fastest rate of growth since 2019. Non-oil GDP growth accelerated to 7.5 percent, indicating broad-based expansion across various sectors that are crucial for employment.

Inflation Under Control

Price pressures eased considerably throughout the year. Headline inflation dropped from 23.8 percent in December 2024 to 6.3 percent by November 2025, the lowest level since February 2019. Food inflation fell by 21.2 percentage points to 6.6 percent, while non-food inflation eased by 14.2 points to 6.1 percent. Inflation on locally produced items decreased from 26.4 percent to 6.8 percent, and imported inflation fell to 5.0 percent from 18.0 percent. This decline in inflation provided much-needed relief to households, restoring purchasing power and easing the burden at market centers.

Interest Rates Decline

Treasury bill rates saw a dramatic drop from above 30 percent at the end of 2024 to around 11 percent in 2025. This reduction not only lowered government borrowing costs but also improved credit conditions for the private sector, fostering a more conducive environment for business.

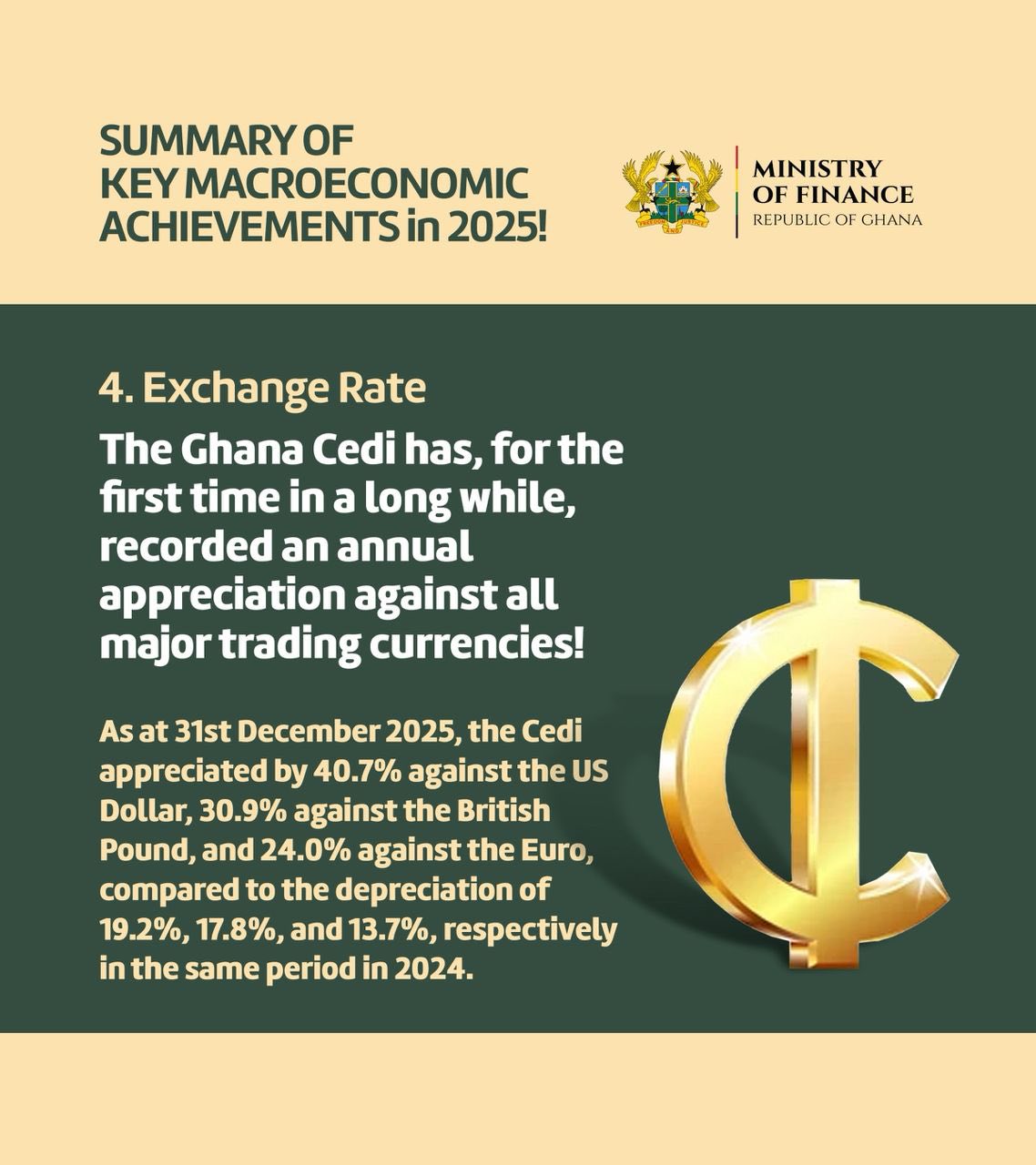

Cedi Appreciation

For the first time in several years, the cedi appreciated against all major trading currencies. It gained 40.7 percent against the US dollar, 30.9 percent against the pound sterling, and 24.0 percent against the euro. This marked a reversal of the steep depreciation experienced in 2024, signaling a stronger currency and increased confidence in the economy.

Strengthened External Position

The trade balance recorded a surplus of US$8.5 billion by the end of October 2025, compared to US$2.8 billion a year earlier. The current account also improved, posting a surplus of US$3.8 billion in the first three quarters, up from US$0.6 billion in 2024. Gross international reserves increased to US$11.41 billion, equivalent to 4.8 months of import cover, reflecting a stronger external position.

Debt Management Success

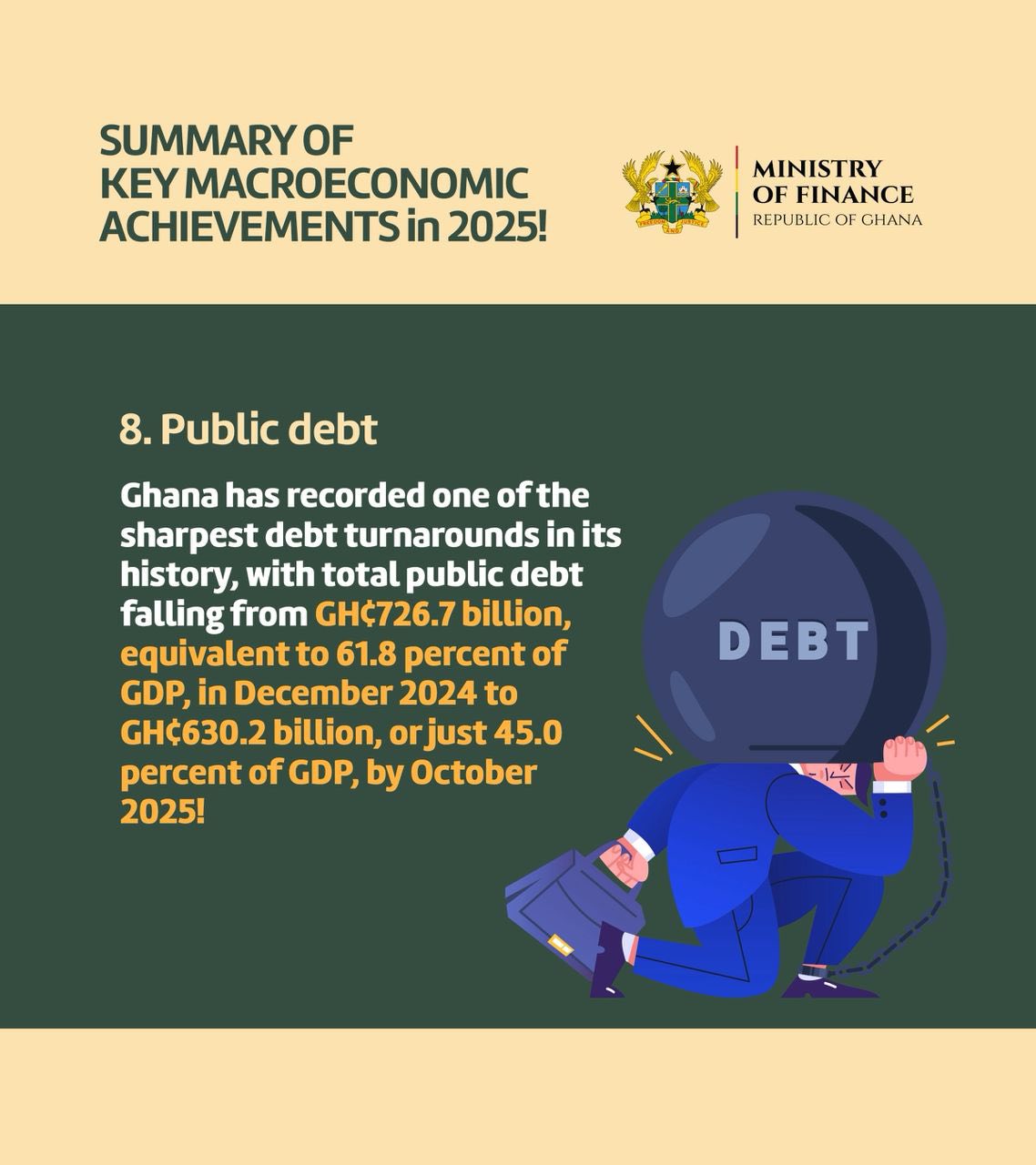

Public debt declined from GH¢726.7 billion, representing 61.8 percent of GDP in December 2024, to GH¢630.2 billion, or 45.0 percent of GDP, by October 2025. This reduction ranks among the sharpest debt reversals in the country’s history, showcasing effective fiscal management.

Investor Confidence Returns

International confidence in Ghana’s fiscal management improved markedly. Fitch, Moody’s, and Standard & Poor’s each upgraded Ghana’s credit ratings, marking the first triple upgrade in several years. This improvement in credit ratings reflects a renewed trust in the country’s economic policies and stability.

Fiscal Discipline Restored

Fiscal performance strengthened as the primary balance recorded a surplus of 1.9 percent of GDP by October 2025, triple the initial target of 0.6 percent. This indicates a commitment to fiscal discipline and responsible financial management.

Pro-Growth Reforms Implemented

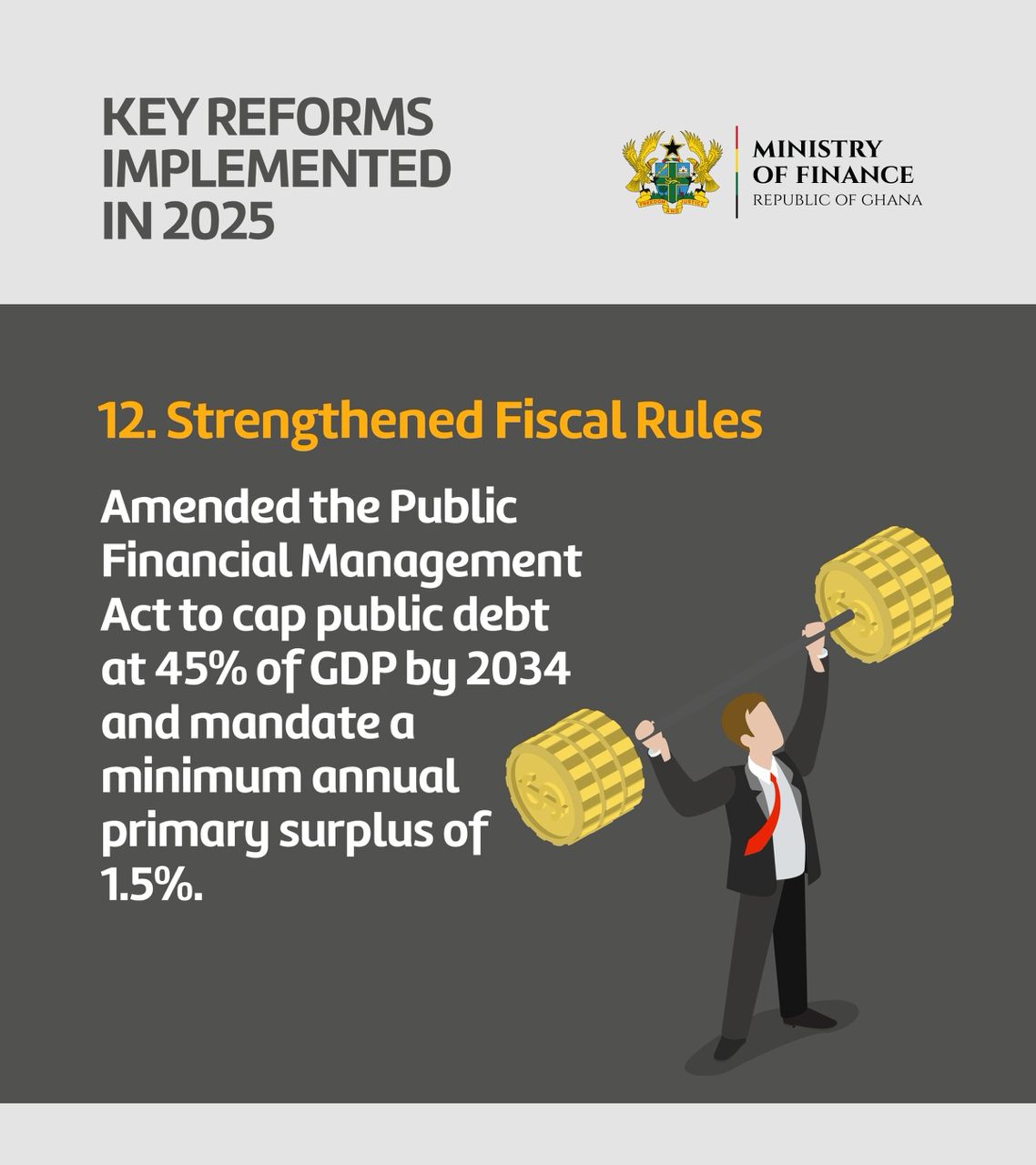

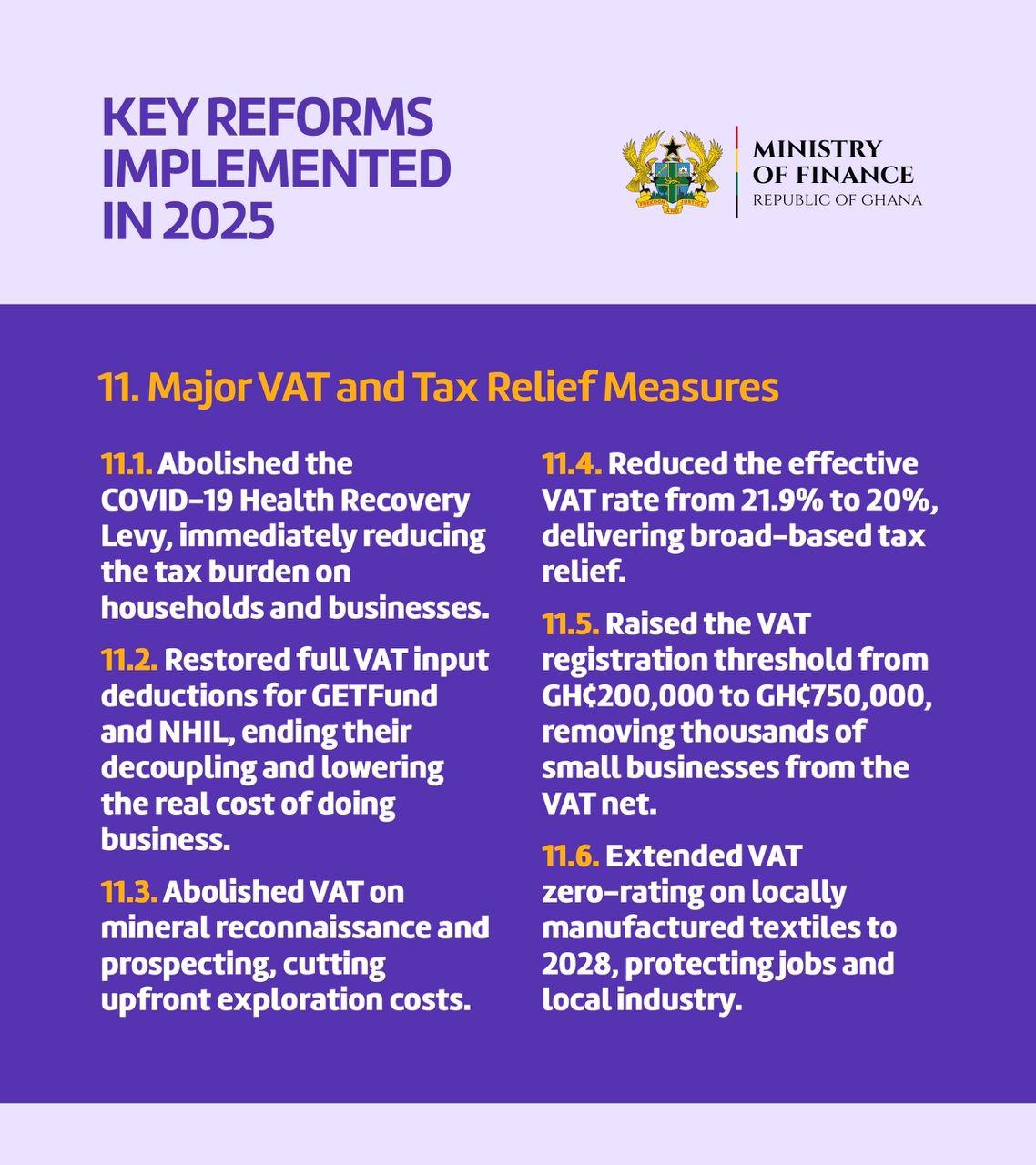

A series of tax and structural reforms were implemented to stimulate growth and ease the cost of doing business. These included the abolition of the COVID-19 Levy, reduction of the VAT rate to 20 percent, restoration of VAT input deductions, an increase in the VAT registration threshold to GH¢750,000, and the zero-rating of textiles to 2028. Fiscal rules were tightened through amendments to the Public Financial Management Act, introducing a debt ceiling of 45 percent of GDP by 2034 and a minimum annual primary surplus requirement of 1.5 percent. Several nuisance taxes, including the Betting Tax, Emission Tax, and e-Levy, were abolished. Oil revenues, mining royalties, and District Assemblies Common Fund transfers were redirected towards priority infrastructure under The Big Push, while at least 80 percent of transfers were channelled directly to local governments.

Financial Sector Reset

The financial sector underwent a broad reset. The National Investment Bank was recapitalised with GH¢1.92 billion, while total funds under management rose to GH¢85.53 billion. The Ghana Stock Exchange Composite Index delivered a return of 27.82 percent, with trading volumes increasing by 146 percent. Fixed income trading rose by 51 percent year-on-year to GH¢108.23 billion.

Looking Ahead

Together, these outcomes reflect a decisive shift in Ghana’s economic trajectory in 2025. The challenge ahead lies in sustaining discipline, deepening reforms, and ensuring that the gains recorded become a durable platform for jobs, growth, and shared prosperity.

{kind=link}