By Joseph BENSON

Ghana’s mobile-money revolution has reshaped how households and businesses transact, save and access basic financial services; yet, as the ecosystem matures, the question is no longer how fast mobile money grows but how the country can expand beyond payments to build the next generation of digital financial infrastructure. This transition will determine whether Ghana becomes a regional fintech leader or remains locked in a low-value equilibrium.

The End of the Beginning: Ghana’s Mobile-Money Transformation

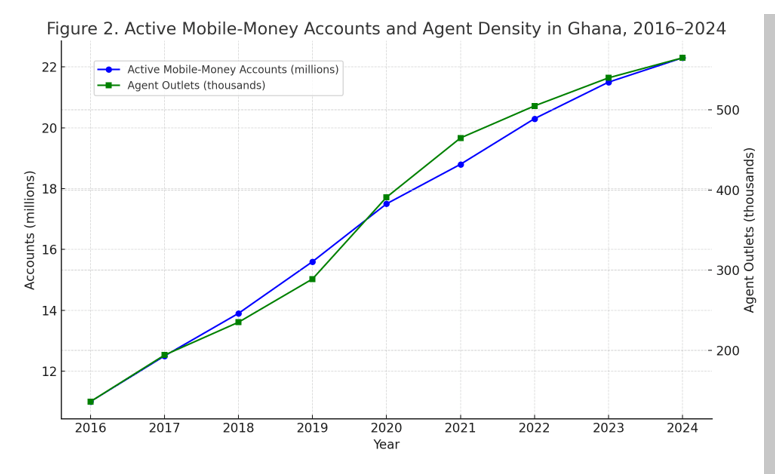

No African country has embraced mobile-money innovation with more consistency than Ghana. Over the past decade, the country has combined strong regulation, deep agent networks and consumer trust to create one of the most advanced digital finance ecosystems on the continent. Mobile-money transaction values exceeded GHS 1.9 trillion in 2023 (Bank of Ghana), representing more than four times Ghana’s GDP. Usage continues to rise, with monthly transaction counts passing 600 million and active mobile-money accounts exceeding 22 million, underscoring the system’s maturity and centrality to daily economic life.

This success is widely recognized. The IMF has highlighted Ghana’s mobile-money architecture as a model of regulatory clarity; the GSMA notes that Ghana is one of only a handful of countries where mobile-money transactions exceed 200 percent of GDP; and the World Bank attributes Ghana’s rapid improvement in financial inclusion, from 41 percent in 2014 to 68 percent in 2021, to mobile money.

Yet the very scale of this accomplishment raises a critical question: what comes next for Ghanaian fintech? Payments are no longer the frontier. They are the foundation upon which higher-value services must now be built.

Beyond Payments: The Strategic Inflection Point

The payments story is well told. Ghana’s next chapter must focus on the value layers that sit atop payments; layers that enable credit access, savings mobilization, merchant digitization, tax compliance and SME productivity.

Across global markets, digital-payment ecosystems become engines of broader financial innovation only when they mature into platforms for lending, insurance, wealth management, credit analytics, and data-driven commerce. Kenya, India and Brazil demonstrate this trajectory vividly. Their models reveal that the long-term economic impact emerges not from transactions but from the economic intelligence that transactions generate.

Ghana stands at this inflection point. The question is whether the country can build a digital financial system that moves beyond payments into deep finance: the suite of services that enable households and firms to borrow, insure, invest, and grow with confidence.

The Merchant Opportunity: Ghana’s Missing Middle of Digital Commerce

Despite Ghana’s payment success, merchant digitization remains uneven. While mobile money dominates peer-to-peer transactions, fewer than 30 percent of SMEs consistently use digital channels for sales, invoicing or working-capital management (World Bank Findex, 2021).

This gap is more than a statistical curiosity. It is a major bottleneck in Ghana’s digital-finance evolution. Without high levels of merchant digitization, payment ecosystems struggle to generate the data needed for SME credit scoring, tax integration, supply-chain automation and fraud analytics. Countries leading the next wave, notably India with its UPI-merchant stack, Rwanda with its interoperable QR infrastructure, and Singapore with its unified merchant API architecture, succeed because they place merchants at the center of their digital economies, not at the margins.

Ghana’s universal QR code system is a strong step forward, but scaling adoption will require a more coordinated push involving telcos, banks, FinTech’s and government procurement agencies.

The Next Drivers of Value: Credit, AI, and Embedded Finance

AI-Enabled SME Credit Scoring

The inability of SMEs to access formal credit remains one of Ghana’s most persistent development challenges. Fewer than 7 percent of Ghanaian SMEs have access to bank credit (IFC), largely because traditional lending models require collateral, financial statements and lengthy approval processes.

AI-enabled alternative credit scoring offers a path forward. By combining mobile-money histories, merchant transaction flows, utility-payment data and behavioral indicators, FinTech’s can construct creditworthiness profiles that expand lending to low-documentation SMEs without compromising risk management.

Emerging evidence from Kenya, Nigeria and India shows that such systems can reduce default rates by 20–30 percent when paired with dynamic repayment structures and real-time cash-flow monitoring. Ghana’s regulatory environment, particularly its structured e-money rules and cybersecurity directives, provides a conducive foundation for scaling responsible AI-driven lending.

Embedded Finance and Sector Integration

Across Africa, fintech’s evolution is moving from stand-alone apps toward embedded financial services integrated into e-commerce, transportation, agritech and health-delivery platforms.

In Ghana, transport platforms such as Yango and Bolt, agri-platforms supporting input-credit schemes, and e-commerce marketplaces increasingly rely on embedded payment and lending solutions. These ecosystems generate industry-specific data that strengthens credit models and expands financial inclusion.

The opportunity now is for Ghana to formalise data-sharing frameworks, expand digital public infrastructure and build the legal foundations for interoperable credit analytics.

Interoperability and Regulation: Ghana’s Structural Advantage

Ghana’s digital-finance regulatory architecture is widely regarded as one of the strongest on the continent. The tiered banking and e-money regime, the Payment Systems and Services Act (2019), strong anti-money laundering (AML) regulations and clear operational guidelines have created an environment where innovation and consumer protection coexist.

Interoperability is the cornerstone of this system. Ghana was the first country in Africa to achieve full mobile-money interoperability, and this foundation is now enabling deeper linkages such as API harmonization, merchant QR universalization and cross-border settlement initiatives under the Pan-African Payment and Settlement System (PAPSS).

As regional blocs move toward harmonized digital markets, Ghana’s regulatory model can become a strategic export.

What Comes After Payments: A Vision for the Next Five Years

Ghana’s fintech future will be determined by its ability to move beyond transaction growth and build a multi-layered digital-finance ecosystem that strengthens SMEs, mobilizes domestic capital and expands productive credit.

By 2030, three developments could reshape Ghana’s digital economy:

- AI-Driven Lending Becomes Mainstream:Fintech lenders use integrated credit analytics, enabling SMEs to access working capital with shorter approval times and lower interest premiums.

- Merchant Digitization Accelerates:Universal QR adoption, digitized supply chains and embedded finance transform SMEs into data-rich enterprises, enhancing productivity and credit access.

- Ghana Emerges as a FinTech Export Hub:With strong regulation and a maturing digital infrastructure, Ghana positions itself as a regional center for payments engineering, RegTech and AI-enabled financial innovation.

The transition is already underway. What remains is a coordinated effort from regulators, industry leaders, universities and development partners to ensure Ghana’s mobile-money success becomes the launchpad for a broader digital-economic transformation.

Joseph Benson is a visionary entrepreneur, business development consultant, and philanthropist based in the United States. With a global network spanning renowned companies, he is deeply committed to fostering innovation and strategic growth across industries

Provided by SyndiGate Media Inc. (Syndigate.info).

{kind=link}